골드만삭스는 "한국은행이 지난 9일 실시한 금리인하에 이어 이날 예정에 없이 0.75%포인트의 금리인하를 발표했다"며 "이같은 금리인하가 경기후퇴(recession)를 피하는데 도움을 줄 것으로 보이며, 상품가격 하락으로 수입 지출이 줄어들 수 있는 점도 원화 강세에 긍정적일 것"으로 전망했다.

아울러 골드만삭스는 2009년 1분기중 최소 또 한차례의 금리인하를 단행할 것으로 보인다고 밝혔다.

에바 이 및 권구훈 애널리스트는 "원화가 단기간 동안 약세 압력에 여전히 시달리겠지만 상품가격 하락에 따른 수입비용 감소로 강세를 보일 것"이라며 "한국은행의 단호한 움직임도 한국 경제가 내년 경기후퇴를 피할 수 있을 것이라는 우리의확신을 높여줬다"고 평가했다.

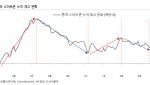

골드만삭스는 "원화가치가 향후 3개월내 달러당 1250원까지 상승하고, 6개월내에는 1150원까지 강해질 것"으로 봤다

Korea Policy Watch: The Bank of Korea cut rates by 75bp

The Bank of Korea (BOK) cut the policy rate by 75 bp in the emergency meeting on October 27, to 4.25% p.a.

The meeting, 10 days ahead of the regular BOK monthly Monetary Policy Committee meeting, came as a surprise to the market and the magnitude of the rate cut is much more aggressive than the market expectation of a 25 or 50-bp cut. The decisive and proactive move by the central bank came in response to the fast deteriorating growth prospects domestically and abroad, as suggested by the slowdown in 3Q2008 GDP growth to 3.9% year on year (yoy) reported on October 24.

We view this as a move in the right direction, and it confirms that the central bank’s dominant concern at this point is growth rather than inflation. The domestic equity index plummeted 20% in the past week, and in the mean time, the concerns over a hard-landing of global growth have intensified dramatically. On the other hand, we also see considerable inflation overhang if the KRW continue to trade at its current level of USD/KRW +1400. On balance, we expect the BOK to undertake at least another 25-bp cut in 1Q2009.

We expect the government to speed up the implementation of large-scale fiscal stimulus and to continue undertaking proactive monetary easing. Although the KRW will likely remain under pressure in the near term, we expect the KRW to strengthen over time on the back of the plunge in commodity prices and expected slowdown in imports.

The global money market stress will unlikely dissipate quickly and the monetary easing today would also not be supportive to the KRW as it would slow down the adjustment in the balance of payments, which could otherwise have happened more rapidly through import cuts and net capital inflows. However, we continue to believe that the KRW/USD has overshot on the downside and expect the KRW to strengthen beyond the near term.

We maintain our USD/KRW forecasts of 1250, 1150 and 1120 on 3, 6 and

12-month horizons.

![[포토]윤석열 대통령 탄핵심판 첫 변론 준비기일 27일 예정대로 진행](https://image.edaily.co.kr/images/Photo/files/NP/S/2024/12/PS24122400433t.jpg)

![[포토]'더불어민주당 원내대책회의'](https://image.edaily.co.kr/images/Photo/files/NP/S/2024/12/PS24122400387t.jpg)

![[포토]국무회의 입장하는 한덕수 권한대행](https://image.edaily.co.kr/images/Photo/files/NP/S/2024/12/PS24122400378t.jpg)

![[포토]은행권 소상공인 금융지원 간담회](https://image.edaily.co.kr/images/Photo/files/NP/S/2024/12/PS24122300609t.jpg)

![[포토]인사청문회 출석한 마은혁 헌법재판관 후보자](https://image.edaily.co.kr/images/Photo/files/NP/S/2024/12/PS24122300404t.jpg)

![[포토]아침 영하 10도, 꽁꽁 얼어붙은 도심](https://image.edaily.co.kr/images/Photo/files/NP/S/2024/12/PS24122300843t.jpg)

![[포토]스케이트 타는 시민들로 북적](https://image.edaily.co.kr/images/Photo/files/NP/S/2024/12/PS24122200317t.jpg)

![[포토]기름값 10주째 올라…전국 휘발유 평균 1652.2원](https://image.edaily.co.kr/images/Photo/files/NP/S/2024/12/PS24122200258t.jpg)

![[포토]크리스마스 분위기](https://image.edaily.co.kr/images/Photo/files/NP/S/2024/12/PS24122200248t.jpg)

![[포토]'서울광장 스케이트장 좋아요'](https://image.edaily.co.kr/images/Photo/files/NP/S/2024/12/PS24122000768t.jpg)

![[포토]안소현-김성태 본부장,취약계증 후원금 전달식 진행](https://spnimage.edaily.co.kr/images/vision/files/NP/S/2024/12/PS24121400036h.jpg)